It’s been almost exactly one year since I updated my list of healthcare venture capital funds with money to invest. I posted updates nine times between late 2010 and late 2012, so a new version is way overdue.

I’ve again included some non-VC firms in the list, as financing can sometimes come as debt, private equity and/or sales-of-future-royalties. I’ve also included some announcements from firms that are no longer investing, as it’s best to identify those firms early.

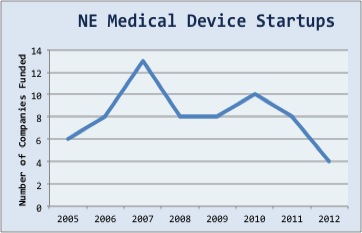

According to PWC’s recent quarterly MoneyTree report, no new medical device companies achieved Series A fundings in New England in either Q2 or Q3 2013. Zilch, zip, zero, nothin’, no, nada.

I’ve been tracking first-time venture financing of medical device companies in Nw England since 2005. You’ll find the link to my latest list of these companies at the bottom of this post. I wish I had a better update to offer.

Like virtually all cataract surgery patients, my parents were thrilled with their cataract procedures. Why not? After a quick office procedure, their new intraocular lenses (IOLs) gave them better vision than they had experienced for more than a decade.

Now imagine a world with no devices for cataracts, only drugs. Imagine taking one or more medications every day for the rest of your life – drugs which could not cure cataracts, but which slow the inevitable progression towards blindness. Imagine the typical chronic-medication side effects: somewhere between minor discomfort and an increased risk of cardiovascular mortality. How does that sound?

When given a choice, I’ll take medical devices over drugs every time. Here’s why.

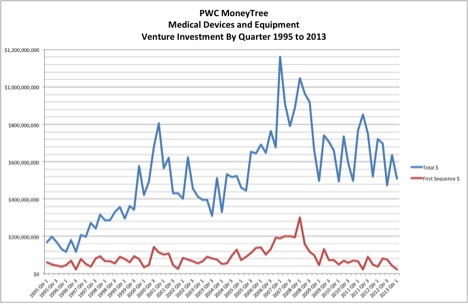

The latest quarterly MoneyTree Report was just released, providing some insight into the state of medical device venture funding in the US. I downloaded and plotted the historical trend data for medical device VC investments in the U.S. from Q1 1995 to Q1 2013. Click on the thumbnails for larger images.

If you haven’t learned to fear adhesive bonds, you haven’t lived a complete medical device life. Adhesives are truly marvels of transmutation: liquids stay liquid until they magically become solid, and a drop or two of base substance can hold dissimilar materials together with superhuman strength.

Yet control of adhesive processes is always a nightmare. UV fluence or position changes from lamp-to-lamp, and oven temperature varies seasonally. The environment is always too damp or too dry. Dispenser accuracy varies. Somehow the location of your adhesive on today’s device has shifted slightly from last year’s location. With adhesives, you just never know which variable is going to cross the line from in-control to out-of-control. You don’t need a masters in statistics to see that a large number of low-probability process failures adds up to a higher-than-desirable probability of bond failure.

I routinely bore people with my assertion that everyone should be required to study and master statistics in high school. We all need statistics to better understand the world we live in and the news we read. Without statistics literacy, we can easily be misled. In our personal lives, we make financial investments, buy insurance, and make decisions with risks. At work, engineers and scientists need statistics to understand designs, processes and experiments. Sales and marketing people need statistics to understand market attractiveness and sales probabilities. Supply chain and operations experts need statistics to understand forecasts, materials plans, and manufacturing processes. Even accountants and finance types need statistics to understand currency risks, stock options, and financial instruments.

In the eight years of data I’ve collected on New England medical device company venture funding, I’ve never seen it this tough. Only four new companies were funded in 2012 (see my complete list below).

You might be tempted to blame VC belt-tightening or the “Patient Protection and Affordable Care Act.” You’d be wrong. While the macro environment has its challenges, four new NorCal medical device startups were funded in Q4 alone.

Ask most medical device marketers about market segmentation, and you’ll get an earful about physician specialty (and subspecialty), hospital/facility size or type (academic, ASC, for profit, large system, etc), or adopter type (early adopters, followers, and skeptics). Unfortunately, these approaches rarely help companies identify customer groups that are differentially addressable – i.e. best served by different products or services, different price points, and/or different marketing channels and sales techniques.

Contrast the typical medical device approach to the sophisticated techniques of consumer product firms. Are you a Barry, Jill, Buzz, Ray, or Mr. Storefront? Best Buy’s in-store staff segments you with a few questions before steering you to the products you’re most likely to want. Amazon suggests possible purchases for you, based on your clicks plus the buying history of other customers who bought the same products you did. Target buys your demographic data to combine with your Target purchase history to create custom coupons for you.

Medical device firms can do much, much more to understand and better serve their markets. Even back in the 1980’s much more could be done. Let me explain how I approached market segmentation twenty-something years ago.

Technically creative product designs stoke engineering pride. Most medical device engineers are happiest when flexing their technical muscle – developing elegant mechanisms, designing clever electrical circuits, and writing creative code. Technical muscle grows stronger with every new product developed.

Strong technical muscle alone doesn’t make a medical device engineer a star. A great attitude is necessary too, but still not sufficient. Star medical device engineers also develop several other muscles needed to bring great products to market. One critical strength is the ability to develop great engineering specifications and tests.

The glass is half full. I’ve been tracking the fundraising activity of healthcare venture firms for the last few years, and I estimate that there are about 250 VC firms actively investing in healthcare innovation worldwide. In contrast, a list I created ten years ago, at InfraReDx, included about 500 healthcare VC firms. Times are tight in 2013.

Technically creative

Technically creative